It was always going to be a matter of time before the ‘rehabilitation revolution’ was down-classified to an ‘evolution’ (Justice Committee, 2013). A year on from the launch of the Transforming Rehabilitation (TR) agenda the political, financial and cultural complexities are showing signs of reining in any über-aspirational claims as to its scale or speed.

It has taken a strong dose of (r)evolutionary impetus to focus minds. For many decades prisons and probation have evaded any explicit obligation to be judged on actual rehabilitative outcomes. Reoffending rates, especially for those on short sentences, have changed little, perpetuating a conventional wisdom that there is little or no correlation between the performance of these institutions and the propensity of offenders to reoffend (Bastow, 2013a).

Plans to create a market for rehabilitation have sought to turn this systemic fatalism on its head. The first is that a market can offer an alternative and self-sustaining source of innovation, competition and investment. The second is that a market can absorb the risk and costs of any failure. The reality however is showing the inherent limitations of both.

Innovation, competition, and oligopoly

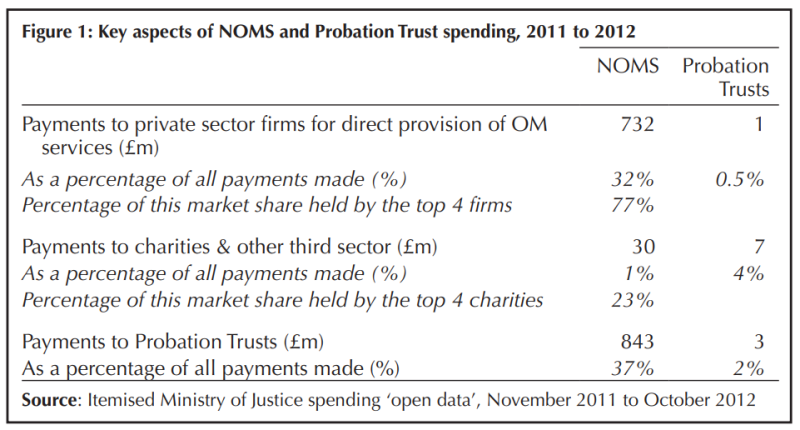

The current offender management (OM) ‘market’ provides some indication of constraints on innovation and competition. As Figure 1 shows, by 2011 around 32 per cent of all outgoing expenditure by the National Offender Management Service (NOMS) was to private firms for OM services. This market has grown into a mature oligopoly. Four private firms (G4S, Serco, Sodexo, and GEO Amey) account for no less than 77 per cent of all payments. By comparison, only one per cent of all payments by NOMS were made to charities, and here the four largest charities accounted for only 23 per cent in this category.

Are there early signs of similar concentration of providers in the bidding line-up for the new Community Rehabilitation Companies (CRC)? With 21 contracts, it is unlikely that we will see similar oligopoly as the existing OM market is dominated by capital-intensive contracts for privately-managed prisons. Ministers, too, have been quick to prioritise innovation in the new set-up. In 2013, Chris Grayling, Minister for Justice, claimed that he was ‘strongly attracted’ by the prospect of innovative partnerships between different types of providers – not just large firms (Justice Committee, 2013).

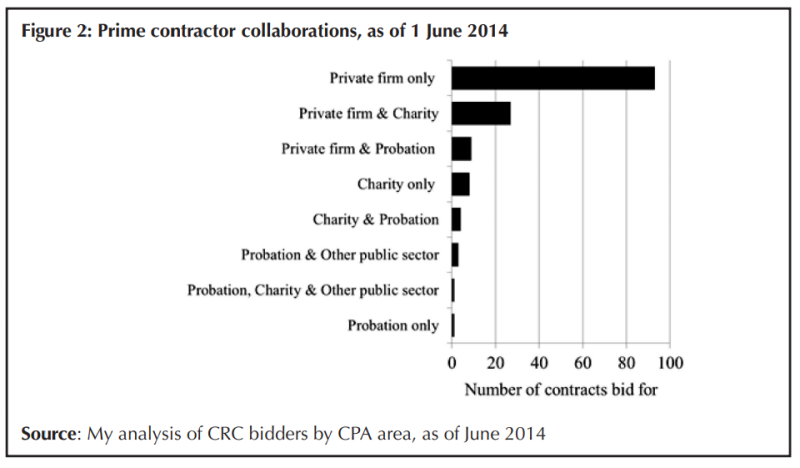

Yet analysis of the prime contractors in the running as of May 2014 still shows strong dominance of single-firm bidders in comparison to other more mixed or innovative configurations. Figure 2 shows that there are 93 cases in which single firms are prime contractors, compared to 53 ‘mixed bidder’ cases. Only 17 out of 146 cases do not involve private sector partners.

There are only 17 instances of former Probation Trusts bidding as part of new consortia with other firms or charities. Of the nine instances in which firms have partnered with staff ‘mutuals’ from Trusts, no less than six see the firms involved bidding unilaterally for the same contracts in the same areas. This indicates early strategic ‘hedging of bets’ by large providers.

Fallacy of risk transfer

A second fallacy is that the market will absorb service failure. Ministers and policy makers have become keenly aware of this over the years, accentuating a bureaucratic tendency to hold on to as much control as possible (Power, 2005). Certainly the extensive architecture of monitoring that has developed on top of the existing private prison system makes these prisons, in many ways, more (not less) accountable than their public counterparts. This is not to say that there are not still glaring frailties in contract monitoring, as last year’s G4S and Serco fiascos have so disturbingly illustrated (National Audit Office, 2013).

Neither are policymakers unaware of the risks involved in dismantling a professional probation system and replacing it with a market. There are already signs in the creation of the new National Probation Service (NPS) of this bureaucratic tendency to control and upwards-absorption of resources. As Figure 1 shows, the cost to NOMS of running Probation Trusts was previously around £843 million.

This money will now be available to fund the new market. Yet the annual running costs of this new body are projected at a staggering £400 million, nearly one half of the previous Probation Trust budget. Rather than freeing up resources to encourage innovation in the market, we risk creating an even more top-heavy bureaucracy.

The rationale put forward for this is that the new NPS will look after the highest risk offenders while these consortia will deal with low-risk offenders. But as officials have pointed out, ‘some people’s risk profile […] will change, so people will move in the direction of the NPS’ (Justice Committee, 2013). It is foreseeable that caseload pressure on the NPS will increase as repeat offenders move up the risk ladder, thus transferring the risks/costs from the market back up to the state.

There is equally apparent affordability pressure downwards on the market to carry out the ‘standard business’ of implementing sentence requirements handed down by the courts. The implication here is that the market will be able to absorb these ‘business as usual’ costs as part of the gains that they make in delivering reductions in reoffending. It seems more likely that contracts will be set up on a more straightforward ‘payment for standard service’ basis, and that the more ambitious payment by results (PbR) element will be delayed until at least after the 2015 General Election. The danger is that we end up with rather similar looking contractual mechanisms in place at the end of it all – without much in the way of savings or reduced reoffending. In the process, we will have decimated a professional probation service.

So the affordability ‘squeeze’ works upwards and downwards. The market is expected to carry out business as usual plus extra PbR elements, but with only half the resources previously provided. It is also unlikely that the resources from an already stretched prison system can be reallocated unless the prison population reduces significantly in the next five years.

There is also the risk that the prison system itself continues to regard rehabilitation as something that ‘happens elsewhere’. Indeed, the Justice Select Committee expressed ‘doubt about the Prison Service’s capacity to implement the changes required under the TR Strategy designed to reduce reoffending rates’ (Justice Committee, 2013). It is difficult to change many decades of cultural fatalism after all – particularly as resource cuts squeeze prisons and an absurd expectation persists that the system is run continuously at close to 100 per cent capacity (Bastow, 2013b).

Prospects for transformation

Public sector reform on this scale requires political artistry. Even after one year, tensions are plain to see, as well as familiar patterns of optimism bias and sub-optimal adaptation as pressures come to bear. The prospects for a truly mixed, innovative and competitive market for CRC contracts seem limited given the early signs of single contractor dominance in the bidding. If ministers are serious about encouraging innovation and competition, then it is likely that they will have to opt for most innovative consortia bids, even if they are not the cheapest or come with the most optimistic projections on reducing reoffending.

Of course, market freedom in this sense conflicts with the management of ‘risk’ and the temptation to replace old bureaucratic structures with even more expansive new ones.There are also strong affordability pressures on the market, and it seems far too optimistic to hope that PbR mechanisms will be sufficient to cover any affordability gap. If the aim is to encourage innovative and successful new markets, it will be necessary to nurture this growth, fund it properly, and counter-intuitively for government, allow the providers involved the flexibility and freedom they need to innovate.

Dr Simon Bastow is Senior Research Fellow, London School of Economics

References

Bastow, S. (2013a), Governance, performance, and capacity stress. The chronic case of prison crowding, London: Palgrave Macmillan.

Bastow, S.(2013b), Rehabilitation outcomes will be limited unless we resolve geographical imbalances in prison capacity, LSE British Politics and Policy blog: http://blogs.lse.ac.uk/ politicsandpolicy/archives/38514

Justice Committee (2013), Oral Evidence for ‘Crime Reduction Policies: A coordinated approach? Focusing on the Government’s Transforming Rehabilitation reforms (Twelfth report), 4 December, London: The Stationery Office.

Justice Committee (2014), Crime reduction policies: a co-ordinated approach? Interim report on the Government’s Transforming Rehabilitation programme (Twelfth report), London: The Stationery Office.

National Audit Office (2013), The Ministry of Justice’s electronic monitoring contracts Report by the Comptroller and Auditor General HC 737 Session 2013-14, 19 November 2013, London: The Stationery Office.

Power, M. (2005), Organizational responses to risk: the rise of the chief risk officer, in Hutter, B. and Power, M. (eds.), Organizational Encounters with Risk, pp. 93-131, Cambridge: Cambridge University Press.