Since 2007, when the credit crisis began to reveal itself, ‘The Banks’ have hardly been out of the headlines. Bailouts, bonuses, LIBOR, sanctions-busting, money laundering, cartelisation, and insider trading are among the seemingly endless litany of scandals which have come to light in the sector. At the same time, political rhetoric has sought to portray the retail businesses of financial services companies as the ‘clean’ or ‘safe’ (‘good’) sector of banking – in contrast to the ‘bad’ risk-hungry, profit-maximising investment banking divisions which are now synonymous with the worst excesses of casino capitalism. Thus in the UK (and the US), the key regulatory response to the financial crisis has revolved around efforts to separate these two parts of financial services – albeit that Andrew Tyrie, the Conservative Chairman of the Treasury Select Committee, has recently said of the proposed UK fencing that it is ‘so weak as to be virtually useless’ (Armistead, 2013).

In any case, the retail parts of these businesses are far from clean: consumers of financial services firms have been victims of three recent waves of offences in the UK, involving many of the same (wellknown) financial services companies, since the deregulation of the sector marked (notably, by the Financial Services Act 1986). Each referred to euphemistically by the anaesthetising term ‘mis-selling’, these are best viewed as systematic theft and fraud though – with the opportunity structures for these crimes created by governments.

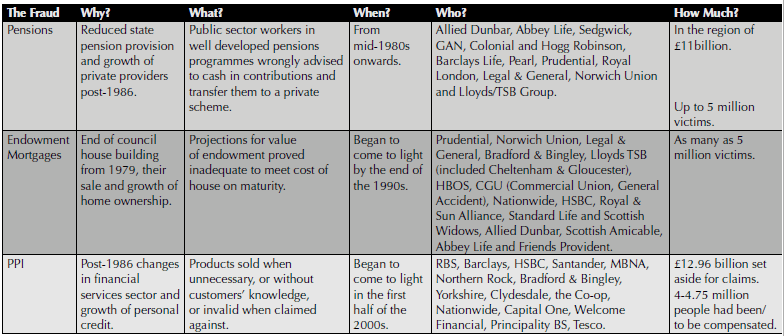

Pensions mis-selling

Even the briefest overview of each of these waves of ‘mis-selling’ – which this article attempts to provide – reveals their similarities. The first of these – widespread pensions misselling – had its origins in the gradual withdrawal of government support for state pension provision, coupled with deregulation of the retail financial services sector in the UK in the latter half of the 1980s. Pensions providers launched into a hard sell, targeting public sector workers in well-developed pensions programmes, advising many to transfer their contributions to private schemes about which they provided false and misleading information. Less than one in ten pensions companies had complied with legal requirements when originally advising on these pensions transfers (Black, 1997). By the end of the 1990s, the then new regulator, the Financial Services Authority (FSA), was estimating the final costs as some £11 billion with up to five million victims (The Bevin Society, 2002).

Indeed, despite the establishment of a timetable for reviewing and if necessary compensating for cases, the pensions providers consistently missed deadlines, ignored regulatory cajoling, and proved relatively impervious to government threats. While breaches had been first uncovered in 1990, in 1997 Economic Secretary to the Treasury Helen Liddell began resorting to consistent but apparently fruitless efforts to ‘name and shame’ the most recalcitrant offenders, with the first such list of 24 companies including Allied Dunbar, Abbey Life, Sedgwick, the French insurer GAN, Colonial and Hogg Robinson, Barclays Life, Pearl, Prudential, Royal London, Legal & General, Norwich Union and Lloyds/TSB Group.

Endowment mortgages and PPI

Then, at the end of the 1990s, another – uncannily similar – series of frauds began to emerge in the sector. The endowment mortgage frauds were based on advisers’ claims that, on maturity of an endowment policy, the sum returned to an investor would pay off the costs of their homes, and likely leave a surplus balance. But such projections often proved to be false. The risk entailed in such products – which were cheaper for home-buyers, but paid off interest only with any maturity value based upon the performance of an investment product – was not adequately communicated to many of the millions who bought them. Again, the companies mired in the endowment mortgages episode were virtually all of the main high street providers of financial services. And, six years after the scandal was first uncovered, the FSA begun, in July 2005, to investigate further ‘the procedures of 52 firms which accounted for 90 per cent of all the endowment mortgages that have been sold’. It claimed that this led to 75 per cent of rejected claims being re-adjudicated in favour of the customer (BBC News Online, 2006).

The same pattern that characterised the pensions and endowment mortgage frauds was then repeated in the Payment protection insurance (PPI) policies that were widely sold at the start of this century. Financial services firms sold customers who had taken out financial products such as mortgages, credit cards or loans a form of insurance in the event of not being able to make payments. Again, these products were often sold when they were unnecessary, or without customers’ knowledge, or indeed were to prove invalid in the event of customers claiming against them. In 2005, the Citizens Advice Bureau (CAB) filed a ‘super-complaint’ to the Office of Fair Trading, by which time the FSA had ‘already fined several smaller firms for mis-selling’ (Neville, 2012); yet some 16 million PPI policies have been sold since 2005 (Pollock, 2012). Meanwhile, only in 2011 did the trade-body – the British Bankers Association – abandon a legal challenge to an FSA ruling on compensating victims. The companies embroiled in the misselling of PPI included many of the, by now, ‘usual suspects’ (ibid). Again, the Financial Ombudsman Service has dealt with hundreds of thousands of complaints from consumers whose claims for compensation have been turned down by companies. By the end of 2012, £12.96 billion had been set aside by companies to deal with compensation claims, with an estimate of 4 to 4.75 million people having been, or due to be, compensated. Yet even in January 2013, the Financial Ombudsman expected an annual tripling of complaints to be dealt with as companies, in the words of the deputy Ombudsman, ‘continue to frustrate their customers with delays and inconvenience’ (Bachelor, 2013).

Corporate theft and fraud in the UK retail financial services sector

Costs

These are not victimless crime waves. Even where victims are (eventually) compensated, such frauds have significant economic and social costs. They generate costs of ‘regulation’, as well as general legal and political scrutiny. There are costs to complainants and victims, both through the creaming-off of percentages of compensation by a new, ravenous area of the financial services sector itself in the form of claims management firms. Further, the discovery of the inability to pay a mortgage, for example, generates emotional and psychological costs. The companies themselves are likely to pass on the costs of compensation to those most likely to be charged for general banking services – which, itself, may entail a class based element, since bank charges are more likely to be incurred by those maintaining the smallest deposits. Moreover, as banks hoard cash to meet future compensation claims, they represent a dysfunctional sector in a context where politicians of all stripes urge greater lending. Perhaps worst of all, the litany of systematic theft briefly reviewed here may generate the perhaps rational public response that ‘they are all at it’, generating political apathy and resignation.

And we will see further categories of mis-selling which will only serve to underscore the fact of long-term, systematic, widespread, routine fraud on the part of the industry. Amongst the contemporary candidates for the next major mis-selling scandal are those which bear a remarkable similarity to the waves of mis-selling reviewed above – for they will include further mis-selling of pensions, mortgage and credit card identity-theft protection. All of those potential scandals already share the same characteristics of the cases we have described here, and all involve the same rogues’ gallery of household name companies.

Steve Tombs is Professor of Criminology, The Open University.

This article is republished from Issue 94, November, 2013

References

1. Armistead, L. (2013), ‘Andrew Tyrie: bank reform legislation “so weak as to be virtually useless”’, The Telegraph, 8 July.

2. Bachelor, L. (2013), ‘PPI payouts expected to rocket in 2013’, The Guardian, 10 January.

3. BBC News Online (2006), Endowment firms pay £120m extra, 11 December, http://bbc.in/13ac1G3

4. Black, J. (1997), Rules and Regulators, Oxford: Clarendon Press.

5. Neville, S. (2012), ‘Scale of PPPI mis-selling overtakes private pensions scandal, says Which?’, The Guardian, 1 November.

6. Pollock, I. (2012), ‘Q&A: PPPI claims – how high could they go?’, BBC News Online, 5 November, http://bbc.in/14f6RUF

7. The Bevin Society (2002), ‘Editorial. Pensions’, Labour and Trade Union Review, http://bit.ly/14f7e1l